Commercial builders’ biggest concerns

Dive Brief:

- Cybersecurity threats, cost overruns, high interest rates, labor shortages and an economic downturn dominate the concerns of the construction industry, according to a report from QBE North America, an insurance company based in Sydney, Australia, with U.S. headquarters in New York City.

- The report surveyed 500 commercial general contractors and construction managers between March 11 and March 24 to identify the primary risks threatening the success of commercial construction projects, according to Ryan Powers, senior vice president and head of construction at QBE North America.

- “The top risks keeping respondents up at night are also the risks they are least prepared for,” said Powers. “Therefore, the findings in the report suggest a gap between awareness of risks and readiness to mitigate them.”

Dive Insight:

The results of the report suggest while respondents are worried about these exposures and threats to their business, they also remain least prepared to manage the potential impact and loss from these very same concerns.

The survey’s findings ring especially true for smaller to mid-sized construction firms, which often operate with less financial capacity than their larger counterparts.

Such companies may have neither the resources to address certain exposures nor the financial reserves to absorb the disruption and losses, said Powers.

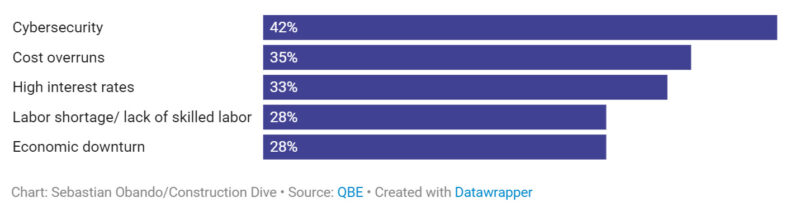

About 42% of survey respondents highlighted cybersecurity as the industry’s top risk, making it the biggest worry for contractors. Other concerns in the top five included cost overruns, high interest rates, labor shortages and an overall economic downturn, according to QBE.

The risks that respondents are most worried about

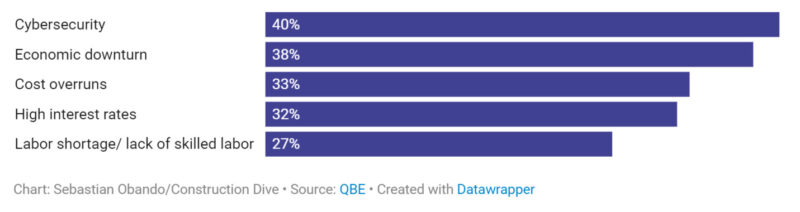

These also make up the same risks respondents feel least prepared for and most vulnerable, according to the report.

The risks respondents are least prepared to mitigate

Bolster cyber defenses

Employees need to know how to recognize potential cyber threats and how to report them, construction executives focused on this area say.

Karen Higgins-Carter, the chief information and digital officer for Providence, Rhode Island-based Gilbane Building Co., recently highlighted phishing and third-party software providers as specific areas of risk for contractors. Firms can limit their cyber risk exposures by proactively training workforces to adhere to cybersecurity best practices, first and foremost, according to the QBE report.

Companies should also work closely with their information technology support to identify vulnerabilities and regularly update software and operating systems. Collaboration with technology, insurance and legal partners for support and guidance is also important.

Labor shortage continues

With no end in sight regarding labor shortages, some companies may be faced with hiring inexperienced workers.

But hiring workers who lack the appropriate work experience can lead to an increase in injuries, quality issues and equipment damage. In New York City, for example, construction injuries jumped 25% from 2022, the second highest amount of total injuries since 2015.

That raises the potential for liability exposures to increase, according to the report.

To mitigate this, Powers recommends strong hiring practices to ensure employees and subcontractors have the necessary credentials. This includes a comprehensive orientation of the work environment, a safety plan review, onsite training and regular check-ins to monitor progress.

Navigating financial conditions

High interest rates are impacting current attempts to bring projects to the market. Owners and developers tend to show caution in investment during periods of high interest rates, said Rachel Personius, associate director at Currie & Brown, a London-based project management firm with a U.S. principal office in New York.

Along with high interest rates and labor costs, materials prices also continue to soar. For example, a combination of inflation and energy costs recently pushed construction input prices up 0.5% in April. That marks an increase in input prices for every month of 2024 so far.

To account for these financial uncertainties, companies should closely review budgets, get ahead of cost overruns on current projects and add contingencies into contracts on future projects, according to the report.

“There are a multitude of risks confronting the commercial construction industry, with new challenges emerging,” said Powers. “Mitigating the potential impact of these risks requires an ongoing commitment and proactive measures to ensure a more efficient, safer and resilient future.”

https://www.constructiondive.com/news/top-concerns-commercial-builders-2024/717474/